Uber vs. Lyft: The Best Stock to Purchase Now

Uber (UBER -0.74%) and Lyft (LYFT -1.15%) are both ride-hailing services. Uber is the market leader in the United States and numerous other countries, while Lyft is a small player that exclusively operates in the United States and Canada.

Uber also delivers food and other products through Uber Eats, while Lyft exclusively provides deliveries through third-party partners like DoorDash. Additionally, both organizations offer electric scooter and bicycle rentals in specific cities.

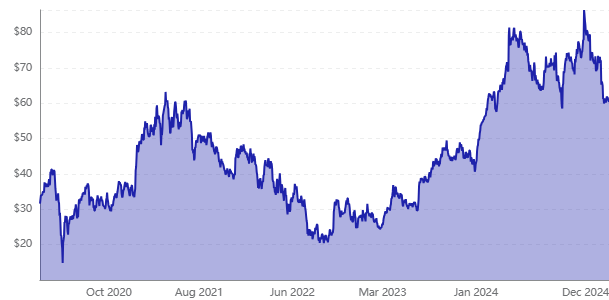

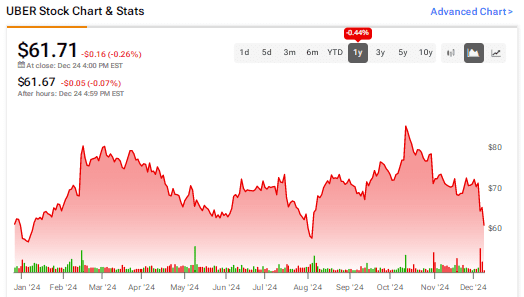

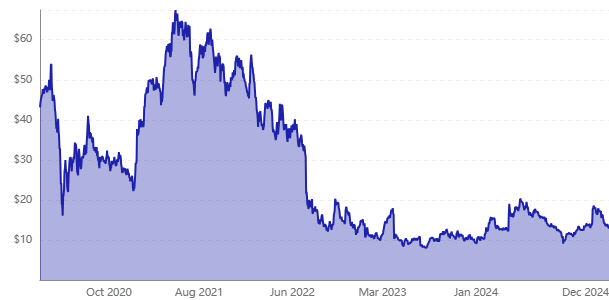

In 2019, Uber and Lyft both went public. At the time of this writing, Uber’s stock is trading at a 36% premium to its IPO price of $45, while Lyft’s stock has plummeted by over 80% from its IPO price of $72. Uber’s investors were impressed by its ability to streamline its operations and capitalize on economies of scale. Conversely, Lyft’s smaller operation encountered persistent losses and lethargic growth. For the foreseeable future, will Uber continue to be a more advantageous investment than Lyft? In order to determine this, we should conduct an in-depth examination of both ride-hailing companies.

The company that is growing the fastest?

Between 2018 and 2023, Uber’s gross bookings grew at a rate of 23% per year, while its revenue grew at a rate of 27% per year. It went from having 91 million monthly active platform users at the end of 2018 to having 150 million by the end of 2023. Its ride-hailing business slowed down during the pandemic, but Uber Eats helped deliver more food, which helped ease some of the stress.

Uber thinks its gross bookings will go up 17% to 18% in 2024. Analysts think that its total income will rise 17% this year and another 16% in 2025, to $50.6 billion. Uber One, its subscription service, had more than 25 million members in the most recent quarter. It also has Uber Teens, a service that lets parents give their teens permission to ride or get packages delivered, and its enterprise and healthcare delivery services.

Lyft’s sales grew at a CAGR of 15% from 2018 to 2023. It wasn’t until 2023 that it started releasing its gross bookings every year. Around 22.4 million people rode it at the end of 2023, up from 18.6 million at the end of 2018.

Due to the fact that it didn’t deliver food, Lyft had a harder time than Uber during the 2020 pandemic. It also had a harder time than Uber during that crisis finding enough drivers, which made its prices go up on average.

Lyft thinks that its gross bookings will grow about 17% in 2024, up from 14% growth in 2023. In 2025, analysts think its sales will rise 15% to $6.6 billion, up 31% from this year. New features like Price Lock (a paid service that locks in prices to set destinations), Lyft Media (which plays media content and ads in its app and in-car tablets), its delivery partnership with DoorDash, and dozens of updates to its main app have helped it grow recently.

Which business makes more money?

Adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) is a way for both Uber and Lyft to measure their bottom line growth. The adjusted EBITDA for Uber went up in 2022, and it more than doubled in 2023. In 2023, Lyft’s adjusted EBITDA went into the black.

General accepted accounting principles (GAAP) say that Uber started making money in 2023. Its profit went through the roof after it got rid of some of its less profitable non-core businesses, slashed the size of its freight and recruitment departments, and cut costs by a huge amount. That’s what Uber wants to happen. Analysts think that Uber’s GAAP EPS will grow 117% in 2024 and 22% in 2025.

GAAP says that Lyft is still losing money, but the company has been cutting costs to keep its business stable. It also doesn’t want to compete with Uber in any international markets. Analysts think that the business will finally start making money in 2025.

Which stock is the best deal right now?

Even though it’s already 15 times next year’s adjusted EBITDA, Uber’s stock still looks like a good deal. In spite of this, its values are falling because the Federal Trade Commission is looking into Uber One’s subscription policies. The price of Lyft is only eight times next year’s adjusted EBITDA, even though it is not being investigated in the same way.

Uber should be able to get past its recent problems, but at these prices, Lyft might have a bit more room to grow. Even though Lyft isn’t as popular as Uber and is a riskier long-term investment, it might be a better buy right now.